AIA

2015

Annual

Report

02 Letter from Robert Ivy

04 Innovation

Strategic repositioning

Digital transformation

Chapter accreditation

Diversity

Continuing education

06 Driving awareness

I Look Up campaign

I Look Up Film Challenge

08 Advocacy

Year of the advocate

Achieving progress together

Advancing legislation

Construction industry leadership

Collaborating to advance the profession

10 Support

The business of architecture

Mobile management

New contracts & a digital platform

AIA Trust: New, improved

12 Data driven

Business & firm support

Economic indicators

Practice-relevant research

Research initiatives

Building Research Information

Knowledgebase

Contents

14 Sustainability

Design & health research

Materials transparency

Supporting resilient communities

The 2030 Committment

Sustainability in energy

Sustainability partnerships

16 Community

Emerging professionals

Communities by Design

18 AIA Convention 2015

Bringing a profession together

Sustainable convention

20 Recognition

Recognizing excellence

COTE Top 10 for Students

22 Architects Foundation

Addressing local & global needs

National Resilience Initiative

Resilience & reconstruction

26 Financials

p // 12015 ANNUAL REPORT

Letter from

Robert Ivy

2015 was a busy year—a healthier

economy, near-full employment, backlogs

swelled to capacity. And, an AIA remade

as a bold and nimble dynamic network for

our members. This resurgent AIA—fine-

tuned for the 21st century—is already

witnessing results.

Our profession is better understood and

appreciated, the dividend of a persuasive

public awareness campaign. For the first

time in more than a decade a visually

compelling national television message

spoke to the essential role of architects

and architecture in our lives. This AIA

effort alone reached 66 million people.

We leveraged this visibility to millions

more with online ads, amplifying our

message and connecting with critical

new audiences through social media, an

inspiring documentary, and a national

film competition. Members can take

the campaign local, tailoring it for their

hometowns.

We moved audiences from passive to

passionately-engaged.

Our profession has more influence.

AIA advocacy efforts helped persuade

Congress to restore and extend the

179D tax deduction, at once an attractive

business development and practice

management tool. AIAU set a new standard

of quality for delivering online continuing

education, reflected in the 95 percent of

course evaluators who’d recommend it to

a friend. At a record-setting crowd at our

convention, former president Bill Clinton

praised architects for their principled

commitment to address climate change

and hinged success in limiting its severest

consequences on others’ being able to

think and act as we do.

Our profession took effective action. We

made meaningful progress on design and

health, resiliency, and the sustainability of

building materials. Our AIA member-led

inaugural 2015 Resilience Summit and

the second Design & Health Research

Consortium charted courses shaped by

our leadership. And where we need to do

more, for example, increasing diversity in

the profession, we conducted our first-

in-a-decade survey on how gender and

race influence perceptions and equity in

the field.

You are the thread connecting all of the

2015 AIA accomplishments. You are the

AIA dynamic network we’re dedicated to

supporting.

Realizing potential—we strive for it

personally and professionally.

Thank you for another extraordinary year.

Robert Ivy, FAIA

EVP/Chief Executive Officer

“ You are the thread connecting all of the 2015 AIA

accomplishments. You are the AIA dynamic network

we’re dedicated to supporting.”

Robert Ivy, FAIA

p // 2 p // 32015 ANNUAL REPORTTHE AMERICAN INSTITUTE OF ARCHITECTS

Creating Cultural Change, the theme of the 2015 Women’s Leadership Summit, brought more than 300 to

Seattle to develop strategies that better support women in the profession and explore new paths to leadership.

Innovation

“ Diversity and inclusion is a priority of AIA.

We have made progress, but not fast enough.

We have great opportunity now to look at how

to achieve the equity, diversity and inclusion

in AIA member firms through a creative means

and provide a framework for the profession

to act faster and better to meet a growing

demand for architects.”

2015 AIA President, Elizabeth Chu Richter, FAIA

Strategic repositioning

The Strategic Council, our new “think

tank,” helped us become more proactive,

anticipate trends and emerge as a leader

in predictive and actionable research.

In 2015, the Council set out a five-year

Strategic Plan that focuses our priorities.

We’ve begun aligning our operations to

meet the goals of the Plan—to reinforce the

stature of architects, expand our influence,

and demonstrate the role architecture

plays in serving society’s needs.

Digital transformation

The new digital foundation for the 21st

century AIA is nearly completed. The

vision: Transform to provide increased

member value. Every legacy technology,

software and process was scrutinized.

We asked the hard question “why” about

processes. Now we’ve changed and

are working differently on your behalf.

We rejuvenated the member and user

experience across our entire landscape,

enhancing AIA operations by adopting

an “agile” project management approach

to our work. Using agile, we focused on

efficiency, collaboration and learning from

the results. A revamped and mobile-ready

AIA Architect is increasing readership

with open rates consistently higher

than industry average. We streamlined

a cumbersome online member renewal

process, making it easier by eliminating

four unnecessary steps. Online renewals

increased 11 percent. In spring 2016, a

new professional AIA website will deliver

the most compelling and relevant content.

Chapter accreditation

High-quality core member services

focused the work of chapter leaders

throughout 2015. This top Member

Services Resource Task Force

recommendation generated statewide

conversations on streamlining operations

and administration so chapters can

access free resources for higher-

quality continuing education and

communications. Twenty-five states

received grants totaling more than

$315,000 and a member service toolkit

was developed with sample policies and

best practices. All AIA chapters signed

a Member Service Agreement and more

than 30 are considering becoming part

of a state or local chapter. Two hundred

thirty-three were accredited by five

member accreditation teams, ensuring

that members have access to quality

services and resources.

Diversity

The highly successful AIA Women’s

Leadership Summit brought 315

architects, interns and students to Seattle

in a vital show of support for gender

equity. Work–life balance, leadership

opportunities and greater attention to

developing a more diverse pipeline were

among the strategies to better support

women in the profession. In addition,

AIA completed its first diversity survey

in a decade and found much remains

to be done. Now, with data from 7,500

respondents, we are better equipped to

establish programs and deliver results.

Already, a blue-ribbon panel is at work

on an action plan for the AIA Board by

the end of 2016.

Continuing education

Members logged an impressive 1.2 million

hours of continuing education through

the AIA network. Increasingly, more credit

hours are being earned through AIAU, our

new online education platform. In 2015,

we added 75 more rigorously curated

courses, launched a star rating system

to rate and rank the courses allowing us

to retire those that fell short. It’s serious

quality control and it’s working. More

than 95 percent of those evaluating

their courses would recommend them to

a colleague. More classes will be added

to the AIAU portfolio in 2016.

Bold strategies and organizational changes

helped us better support our members and

the profession while expanding architecture’s

reach, influence and impact.

p // 52015 ANNUAL REPORTp // 4 THE AMERICAN INSTITUTE OF ARCHITECTS

Driving awareness

I Look Up campaign

What do you see when you look up?

That straightforward question anchored

the bedrock message of our I Look Up

public awareness effort: Architects and

architecture play an essential role in our

lives. Our first advertising campaign in

more than a decade invited the public to

look up and be inspired by the architecture

that surrounds us and shapes the

identities of our communities.

We made the message mobile—shareable

and scalable across all forms of media.

Television advertising generated 66 million

impressions. Another 5 million watched

our ad through online channels. Overall,

we reached nearly 30 million people across

all communication channels in 2015 and

expanded our social networks more than

15 percent. Thousands answered the I

Look Up question by posting photos of

their favorite architecture to ilookup.org.

It’s a remarkable response that gets to

the heart of the architect’s endeavor to

create community.

I Look Up Film Challenge

To maintain momentum throughout

2015, we produced premium film content,

including a documentary about the life of

sight-impaired architect Chris Downey.

This film grew into the I Look Up Film

Challenge that encouraged participants

to produce a film showcasing a unique

perspective on architecture’s effect on

everyday life. The film challenge pulled a

new, energized audience into the AIA orbit.

Three winners emerged from more than 26

inspiring film entries and were announced

at the opening of the inaugural Chicago

Architecture Biennial. The film challenge

reached two million people, including

300,000 through a social media driven

People’s Choice Awards. The Tribeca Film

Festival’s website featured the winners’

film under the fitting title “Three Short

Films That Will Inspire You to Appreciate

Architecture.”

2015 AIA President Elizabeth Chu Richter, FAIA (center) presented the I Look Up Film Challenge awards

to the three winning teams at the Chicago Architecture Biennial. “These films,” said Richter, “inspire the

world to look up and appreciate the beauty of architecture.”

“The experience of

working on the

I Look Up Film

Challenge changed

my perception of

architecture by

learning about

how much work

and passion goes

into designing a

building. It’s a lot

like filmmaking in

a way—if you do

it right, it feels so

natural and organic

that nobody ever

thinks about how

it’s made.”

Filmmaker, I Look Up

Film Challenge

p // 72015 ANNUAL REPORTp // 6 THE AMERICAN INSTITUTE OF ARCHITECTS

Advocacy

“…eliminating this language would be a significant

setback in the effort to make the nation’s building

stock more sustainable.”

AIA EVP/CEO Robert Ivy, FAIA and Michael Brune, Sierra Club Executive

Director, writing to Congress to oppose repeal of Section 433

>>> SPOTLIGHT

Preserving

2030 goals

The foundation for

reducing greenhouse

gas emissions in public

buildings—Section

433 of the Energy and

Independence Security

Act of 2007—set a

goal that all new or

significantly renovated

federal buildings be

carbon neutral by 2030.

AIA’s 2030 Commitment

championed similar

objectives to reduce the

use of non-renewable

energy sources in

building construction

and maintenance.

When an amendment

was proposed to a

Senate energy bill that

would have gutted

the 2030 target goals,

AIA joined forces with

the Sierra Club and

other organizations

to continue fighting

the move.

Strategic efforts, combined with the collective

voice of nearly 88,000 members, achieved big

wins in federal, state and local governments

and reinforced our commitment to protect the

built environment.

In 2015, ArchiPAC, the AIA federal political action committee, raised more than $130,000 to help AIA

raise its political reach and advocate for policies that move our profession and country forward.

Year of the advocate

Advocating for the profession is a core AIA

tenant. AIA designated 2015 the Year of

the Advocate, recognizing that creating

a culture of advocacy will ensure our

collective voice is considered whenever and

wherever policymakers make decisions that

affect our profession. Within the first week

after being announced, joining members

doubled the ranks of AIA Advocacy

Network. This multi-year initiative included

a new advocacy pilot launched in three

states to help build an effective federal,

state and local advocacy infrastructure. The

increased interest in advocacy attracted

record-setting donations to ArchiPAC,

our federal political action committee. We

raised more than $130,000 to help AIA

expand its political reach in Washington.

Achieving progress together

In response to a major AIA grassroots

push, Congress voted to restore and extend

the 179D energy efficient commercial

buildings tax deduction, enabling

architecture firms to claim a valuable

deduction for sustainable work on public

buildings. AIA built a strong coalition that

includes hundreds of organizations and

businesses to fight an effort to repeal the

2030 energy efficiency targets for federal

buildings.

Our federal advocacy program in 2015

included an initiative to reform how the

federal government hires and compensates

architects who design federal facilities.

This AIA focus spurred the U.S. General

Services Administration to announce

plans to change the competition process

for design-build projects and work with AIA

to better train contracting employees on

how to establish compensation rates for

architects who pursue federal work.

Advancing legislation

AIA continued building bipartisan support

for other federal legislation important to the

profession: The National Design Services

Act to provide student debt relief for

architecture graduates; the Safe Building

Code Incentive Act to encourage states

to adopt building codes in exchange for

increased disaster funding; and the Historic

Tax Credit Improvement Act to preserve

and improve the incentive for undertaking

historic preservation.

Construction industry leadership

AIA staff collaborated with industry

partners and closely monitored issues that

impact how architects work. The AIA policy

team analyzed legislative and regulatory

issues related to liability exposure for

architectural firms, qualifications based

selection, construction administration

and the use of school barricades, among

others. AIA strengthened an already robust

partnership with the International Code

Council, formally agreeing to collaborate

on supporting and advancing the adoption

of modern building codes. Our “One Code”

policy led to continued collaborative

leadership on the development of the

International Green Construction Code,

the IGCC, which, with wide industry

stakeholder engagement, is being

combined with ASHRAE Standard 189.1 to

produce a single regulatory tool for green

construction.

Collaborating to advance the profession

In 2015, members and staff worked

together with the U.S. Department of

Energy (DOE) to develop a single definition

of a net-zero energy building, helping

policymakers and practitioners better

define sustainable design. In conjunction

with the DOE we hosted a workshop where

nearly 100 experts from 60 organizations

envisioned buildings of the future. AIA

staff and member volunteers provided

training to the staff at the Architect of

the Capitol to improve their post-disaster

ability to evaluate facilities, buildings and

infrastructure. We concluded a three-

year cooperative grant with the U.S.

Department of Commerce to help open

international markets to architects, which

featured working-abroad training sessions

for members at chapters in Houston and

San Francisco.

p // 92015 ANNUAL REPORTp // 8 THE AMERICAN INSTITUTE OF ARCHITECTS

Support

“…the only way you can really protect yourself is with a strong

payment plan. I always recommend using an AIA contract.

It itemizes the complete scope of work, materials and

installation costs. If you see flooring show up on the job…,

you could pay them for that. But don’t pay them before you

see the materials show up. And that’s why the AIA contract

is brilliant, ‘cause it really protects you.”

John DeSilvia of the DIY Network’s “Rescue My Renovation”

>>> SPOTLIGHT

Entrepreneur

Summit

In July AIA held the

Entrepreneur Summit, a

two-day event captured

on video that offers

interesting perspectives

on what it means to be an

architect. The takeaway:

An architect’s education

is the foundation from

which to build a practice

or chart a versatile

career path. Conceived

and hosted by 2015 AIA

President Elizabeth Chu

Richter, FAIA, the summit

addressed how architects

can harness potential to

enhance their value to

their firm or better serve

clients and communities.

New ways to apply design

thinking was a major

theme. One architect-

panelist developed

project management

software that became

a separate business

enterprise; another

developed a materials

fabrication business; and

everyone discussed how

to own your story with the

media. Art Gensler, FAIA,

delivered an inspiring

keynote packed with

candid advice on how to

build and run a successful

firm. Gensler’s speech and

a panel on new business

models can be found for

free on AIAU.

The business of architecture

We expanded the tools we provide

members to help them build their

businesses and manage their careers. For

proven firms and those just-launched,

the tools mark new paths to prosperity.

Our vibrant network of Knowledge

Communities added member-to-member

resources, so fellow professionals can

stay on top of practice trends with

whitepapers, webinars and documented

best practices.

Mobile management

Courtesy of the AIA Small Firm

Roundtable (SFRT) and the Young

Architects Forum, members now have

AIAKinetic, a mobile app that connects

small firms to a comprehensive suite of

real-world how-tos and best practices.

The SFRT also assembled a team of

member volunteers to keep the content

timely and relevant.

New contracts & a digital platform

AIA released 10 new documents and forms

in the Design-Build family—endorsed by

the Construction Specifications Institute—

and four new agreements and forms in

our core Conventional family, used for the

design-bid-build project delivery method.

In December, we premiered a digital

platform that improves ACD5 system

performance, ensuring continued ease of

use and building on customer satisfaction

ratings that already exceeded year-end

targets. In 2015 we exceeded one million

document downloads for the second year

in a row and our contracts were touted on

an NBC TODAY show segment “How to

Shop for a Contractor.”

Deeper industry alliances

AIA and the Associated General

Contractors of America expanded their

existing collaboration. Already at work

on shared challenges and education-

related issues, these representatives of

the building team executed an MOU with

the Construction Owners Association of

America, our counterpart in the design

and construction industry, to further

advance common goals. A similar MOU

with ASHRAE, drafted in 2015, takes

effect in 2016.

AIA Trust: New, improved

Practicing architecture implies risk for

career newcomers and veterans alike. AIA

Trust is all about helping manage risk. An

all-new AIA Trust website, launched in

2015, makes resources and benefits easier

to find and better tailored to our member’s

personal and professional needs.

AIA Trust now has white papers on

topics including effective contract

administration, a comparison guide

about professional liability policies,

documentation techniques to protect your

practice and the risks of condominium

construction. Added were four webinars

to help you run a successful practice

and navigate the Affordable Care Act.

Another webinar gives AIA chapters an

overview of insurance needs.

For firm owners with a pending E&O claim

or another legal matter, the AIA Trust

launched the AIA Trust Legal Network in

2015. It is an easy way to identify qualified

A/E construction lawyers who can help

manage an issue. Check out the AIA

Trust’s other resources, from a how-to

guide on starting and running a firm to

the dos and don’ts of ownership transition.

Industry standard tools, product launches and

new services made it easier for architects and

design professionals to do business and manage

risk in 2015.

The AIA Home Design Trends Survey highlights how residential architects are shaping how homes

function, look and integrate into communities. Each quarter, billings and inquiries at more than 600

architecture firms documents the financial health of firms in the residential sector.

p // 10 p // 112015 ANNUAL REPORTTHE AMERICAN INSTITUTE OF ARCHITECTS

Data driven

Quality data, market intelligence, research

and sharp insights equipped members and the

industry to make good business decisions.

Business & firm support

Good decisions require good data. AIA’s

influential Architecture Billings Index ably

predicted the 2015 recovery. The data

appeared in more than 800 articles and

drew coverage by the Associated Press

and Reuters. The AIA Home Design Trends

Survey helped members stay competitive

with quarterly data showing where new

home and remodeling demand converged

with consumer interests.

And the 2015 Compensation Report

added to its already comprehensive data.

The Report covers 39 positions, including

job descriptions, for 27 states, 27 metro

areas and 15 cities. Plus we debuted the

Compensation Survey Salary Calculator

that gives emerging professionals salary

results for 17 positions.

Economic indicators

In 2015, we added two economic insight

tools. A monthly indicator includes

data on employment, construction

spending, housing starts and vacancy

rates. AIA also improved its semiannual

State Economic Profiles, a collection of

national, regional and state employment

and construction data—tools that prove

useful for government advocacy and

media outreach.

Practice-relevant research

A 2015 Research Summit, a joint activity

of the Board Knowledge Committee and

Practice and Prosperity Committee,

brought together practitioners and

members of the Academy to recommend

how AIA can support increased literacy

and use of research. A 2016 roadmap will

augment AIA’s research efforts.

Research initiatives

A jury representing the College of Fellows

and the Board Knowledge Committee

selected four 2015 recipients for the

Upjohn Research Initiative Program

that provides matching funds of up to

$30,000 for applied research projects

advancing design and professional

practice knowledge.

The College of Fellows also awarded

the 2015 Latrobe Prize of $100,000

to a team led by Woodbury University’s

Arid Lands Institute (ALI). The grant will

enable ALI and its partners to develop

and test a proprietary digital design

tool which, when fully realized, will

support communities and design teams

developing and building water-smart

infrastructures and devising and shaping

public policy for drylands urbanism.

Building Research Information

Knowledgebase (BRIK)

This free portal to peer-reviewed

research projects and case studies grew

to 19 contributing organizations in 2015

across government agencies, architecture

firms, academics and research groups. An

additional feature was added: Member-

only access to thousands of journals

through three digital library collections.

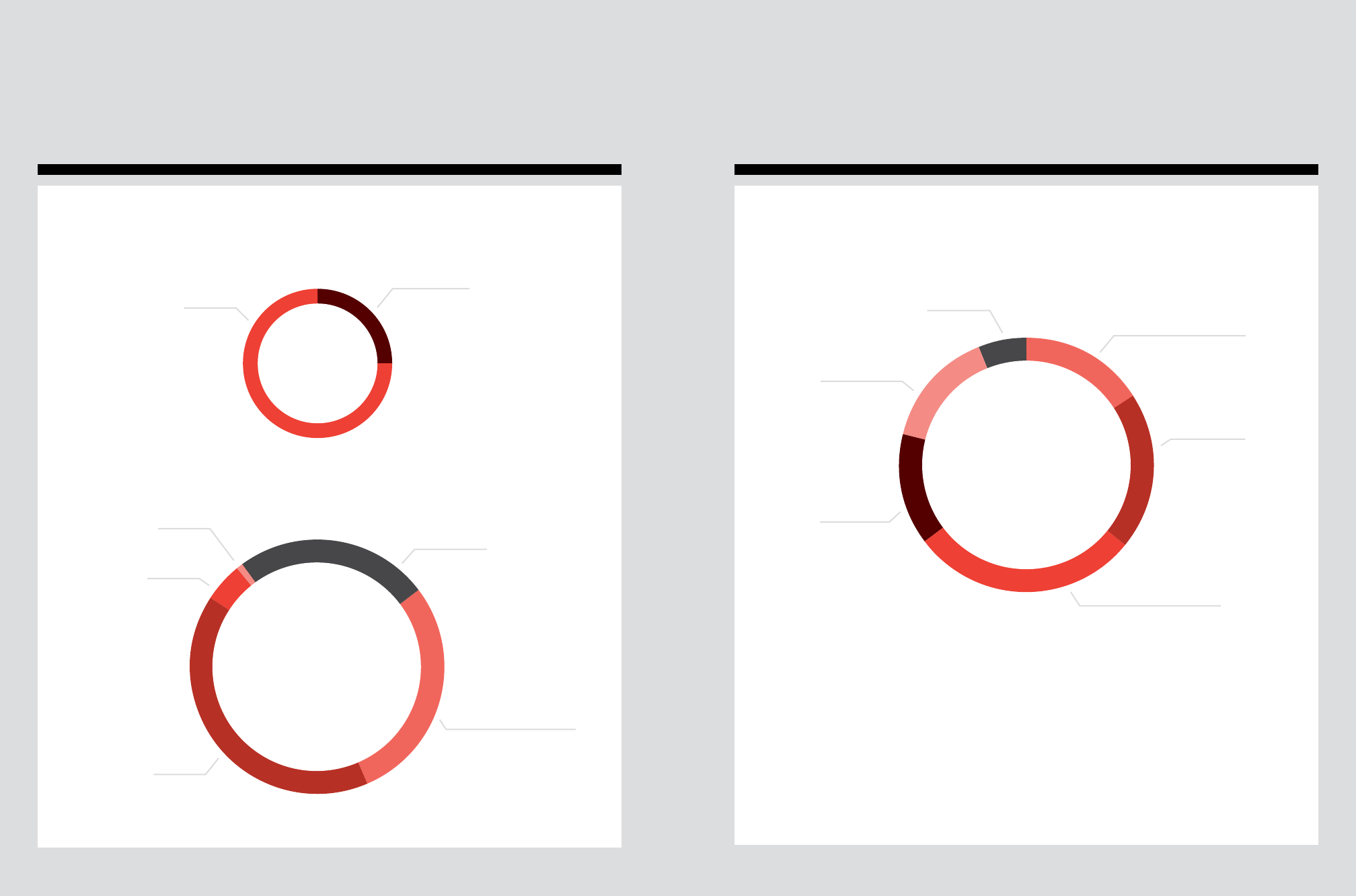

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

ARCHITECTURE BILLING INDEX

NATIONAL REGIONAL SECTOR PRACTICE

ABI

* All graphs represent data from March 2015 – March 2016.

March 2016

The Architecture Billing Index (ABI) is a diffusion index derived from the monthly Work-on-the-Boards survey, conducted by the

AIA Economics & Market Research Group. The ABI serves as a leading economic indicator that leads nonresidential construc-

tion activity by approximately 9-12 months. The survey panel asks participants whether their billings increased, decreased, or

stayed the same in the month that just ended. According to the proportion of respondents choosing each option, a score is

generated, which represents an index value for each month. An index score of 50 represents no change in firm billings from the

previous month, a score above 50 indicates an increase in firm billings from the previous month, and a score below 50 indicates

a decline in firm billings from the previous month.

NATIONAL

Architecture Firm Billings Close Out First Quarter on an Upswing

Graphs represent data from March 2015 – March 2016.

40

45

50

55

60

65

BillingsInquiriesDesign Contracts

Mar-16Feb-16Jan-16Dec-15Nov-15Oct-15Sep-15Aug-15Jul-15Jun-15May-15Apr-15Mar-15

Below 50 =

Above 50 =

50 = No change

from previous

period

55.6

51.9

52.2

52.3

51.3

West:

50.4

South:

52.4

Northeast:

51.0

Midwest:

49.8

REGIONAL

Midwest Firms See Continued Weakness; Firms in Other Regions Report Modest Growth

Graphs represent data from March 2015 – March 2016 across the four regions.

50 represents the diffusion center. A score of 50 equals no change from the previous month. Above 50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

Institutional: 48.0 Residential: 55.7Commercial/Industrial: 51.8

SECTOR

Upswing at Residential Firms and Slide at

Institutional Firms Continue in March

Graph represents data from March 2015 – March 2016 across the

three sectors.

50 represents the diffusion center.

A score of 50 equals no change from the previous month. Above

50 shows increase; Below 50 shows decrease.

3-month moving average.

40

45

50

55

60

Mar-16Nov-15Jul-15Mar-15

PRACTICE

2015 Saw a Mixed Performance Relative to Expectations for Firm Profitability

Units: 2015 profitability relative to firm expectations, % of firms

12.3%12.3%

29.9%

22.6%

23.0%

Significantly exceeded

expectations

Modestly exceeded

expectations

Met our expectations

Modestly underperformed

expectations

Significantly underperformed

expectations

Average compensation for

architectural staff positions

averaged just under

$80,000 at the beginning

of 2015, up about 3.5% from

early 2013 levels, or 1.75%

per year.

2015 AIA Compensation Report

Architecture Billings Index

A leading economic indicator, the Architecture

Billings Index (ABI) provides a nine-to-12 month

lead time between architecture billings and

nonresidential construction spending. It is closely

followed as an indicator of the health of the

construction industry.

>>> EXAMPLE

p // 132015 ANNUAL REPORTp // 12 THE AMERICAN INSTITUTE OF ARCHITECTS

2015 COTE Top Ten Plus award winner: U.S. General Services Administration, Seattle Federal Center South Building 1202. After the

first year, quantifiable metrics showed the facility’s metered energy performance met every design target, including the contractually

required energy performance and the AIA 2030 Committment. Photo Credit: Benjamin Benschneider

Sustainability

We put the power of our sustainability

portfolio to work in 2015, using diverse new

opportunities to improve health, enhance

community resilience, reduce energy use and

promote materials transparency.

Design & health research

2015 marked the first full year of the AIA

Design & Health Research Consortium,

created to strengthen understanding of

links between design and health. The

consortium developed evidence-based

tools for professionals and translated the

findings for policymakers and the public.

Eleven charter members funded research

on everything from the effects of indoor

temperatures on sleep deprivation and

depression (University of Florida) to a

“best design” competition for a mobile

isolation treatment unit to combat the

Ebola epidemic (Texas A&M University’s

Center for Health Systems and Design). Six

universities joined the consortium in 2015.

Materials transparency

In a sustainable built environment,

architects play an important role in

helping clients and communities make

better choices about the health and

environmental impact of building

materials. A working group of architects,

attorneys and insurers was convened to

evaluate risks of this opportunity. The

group worked with AIA’s contract team

to develop a model contract. A Materials

Transparency white paper is also available

on the AIA website.

Supporting resilient communities

Creating resilient communities requires

new and collaborative approaches

among stakeholders. We expanded

our contribution to this effort with the

2015 Resilience Summit that gathered

representatives of government agencies,

scientists, policy experts and the insurance

industry. We examined what makes a

community “resilient” and who holds the

responsibility to ensure it is. The Summit

Report laid out next steps. We are also

assisting AIA chapters participating in

the Rockefeller Foundation 100 Resilient

Cities initiative, providing practice and

policy-focused resources and access to

a digital network where they can share

best practices as they host workshops and

meet with community officials to promote

design as part of making communities

more resilient.

The 2030 Commitment

When firms sign the 2030 Commitment

they support consistent and rigorous

metrics relating to building performance

to achieve carbon-neutral buildings

by 2030. AIA partnered with the U.S.

Department of Energy (DOE) in 2015 to

simplify the reporting process through

the AIA 2030 Design Data Exchange

(DDx), a web-based interface that allows

firms to track and report energy use in

their design projects. It also helps AIA

monitor its own goals. The interface

streamlines the job of reporting data

and enables project information to be

entered in real time. Plus, architects

can use the sophisticated reporting

and research tools to compare building

performance projections with similar

projects. Information about specific

firms, projects and clients remains

completely confidential.

Sustainability in energy

In one example of our effort to increase

energy-efficient design literacy in our

profession, AIA laid out recommendations

at DOE’s 2015 Energy Codes Conference

to increase energy efficiency in existing

buildings. The presentation reviewed AIA’s

work on incentives, energy modeling,

energy-efficiency finance and deep

energy retrofits.

Sustainability partnerships

We partnered with Architecture 2030

and AIA Seattle to launch the AIA+2030

Online Series that provides members

with an interactive, step-by-step guide

to achieving sustainable solutions.

Sharing knowledge is intended to help

professional designers create super-

efficient buildings—and provide firms with

skills to set them apart in the marketplace.

AIA also convened the inaugural meeting

of a broad group of energy-efficiency

experts—the Energy Leadership Group—

to help set the agenda for AIA’s energy-

related activities and provide guidance

on the AIA’s energy policy formation and

activities, including advocacy and code

development and adoption.

“ If architects ask for disclosure of product

contents without explaining why they are asking,

their intent to use that information is open to

interpretation. It is important to be clear with

clients and with the public about the reasons for

seeking and receiving disclosure documents.”

2015 AIA Materials & Risk Summit

p // 152015 ANNUAL REPORTp // 14 THE AMERICAN INSTITUTE OF ARCHITECTS

Emerging professionals

In 2015, we unveiled powerful programs

and alliances to help emerging pro-

fessionals excel. Targeted educational

opportunities, financial support and

creative outlets are mainstays of the effort.

AIA’s 2015 exhibition showcasing the

group’s startling creative talent perfectly

underscores the importance the next

generation of architects.

AIA and the Association of Collegiate

Schools of Architecture hosted an AIA

Convention conference to stress the

link between architectural education and

practice. We also partnered with Black

Spectacles to offer online prep tutorials

for the Architect Registration Exam,

enhancing our support for emerging

professionals on the path to licensure.

And the National Associates Committee

and Young Architects Forum expanded

their reach by helping shape a virtual

leadership event that drew 300 partic-

ipants live-streamed from Washington,

D.C. to AIA chapters in Boston, Cleveland,

Phoenix and San Antonio.

AIA provides ongoing scholarships

to emerging architects, including the

AIA Jason Pettigrew Memorial ARE

Scholarship, now managed through the

Architects Foundation. The Henry Adams

Scholarship dispersed nearly $90,000 to

91 schools and 213 students. AIA awarded

$85,000 in grants to augment existing

AIA chapter scholarship programs.

Another 2015 financial initiative targeted

unpaid internships with the launch of the

Know Your Worth campaign. It featured

two videos, “Value Your Work” and

“Value Our Future,” about the collective

importance of getting paid for internship

hours worked.

Communities by Design

The signature service of the AIA Center

for Communities by Design is bringing

community leaders together with sustain-

able design assessment teams (SDAT)

to help citizens stake a claim to their

future. The work of the design assistance

program harnesses the potential of design

to create sustainable, livable communi-

ties and connects with our deep desire

to help make the world a better place.

The Community Development Society

International heralded the Center as

outstanding in 2015. The award cited

the SDAT program as one that “leads to

enormous changes in local approaches

by combining community engagement,

listening and reflecting, explaining new

ideas and making clear and concise

recommendations that respect and reflect

community priorities in a way that enables

communities to develop frameworks and

comprehensive plans.”

Community

How we serve our communities defines us as an

organization and as a profession. In 2015, the

answers were increasingly rich and diverse.

>>> EXAMPLE

Louisville, KY

An SDAT devised a revitalization strategy for

Russell, a neighborhood where 58 percent

of residents live below the poverty line and

residents face 30 percent unemployment.

About 15 percent of its housing stock is vacant

and crime is five times the citywide rate. The

SDAT suggested an urban design strategy to

reconnect the neighborhood to downtown and

redesign an underutilized state-owned parking

lot into higher-density, mid-rise residential

buildings above restaurant, retail, cultural and/

or entertainment spaces. The team proposed that

the neighborhood create a civic organization and

leverage modest public investments to attract

larger private investment. The community was

enthusiastic. The steering committee chair

remarked, “I simply can’t believe how much work

you were able to complete in just three days.”

Del Paso Heights and SDAT participants discuss the

specifics of a community development plan designed to

establish an economic identity that will promote its viability

to the city of Sacramento.

Sacramento, CA

An SDAT focused on transforming Del

Paso Heights, a struggling neighborhood in

Sacramento. The team called for creating a

Community Development Corporation to

establish an economic identity and promote its

viability to the city. It suggested an urban design

strategy for a town center with new approaches

to housing and retail infill, and public private

partnerships to enhance local infrastructure.

Residents applauded the recommendations. One

said, “I’d like to commend you very highly for

what you’ve done. I didn’t think in three days

much could be done, and you’ve really shown us

a vision of what is possible.”

Residents of Russell, KY hear details of 2015 AIA SDAT

recommendations that, if implemented, will help revitalize

the community.

p // 172015 ANNUAL REPORTp // 16 THE AMERICAN INSTITUTE OF ARCHITECTS

AIA Convention 2015

It was one of our best, most inspiring and most

impactful events yet, bringing thousands of

architects and design professionals to Atlanta

and setting a few new records.

“ To the extent that we’re going to avoid the

worst consequences of climate change, we are

depending on [architects] and people like you,

and those who begin more to think like you,

about how to design the environment in which

we live and work.”

Former President Bill Clinton, Day 1 keynote

Bringing a profession together

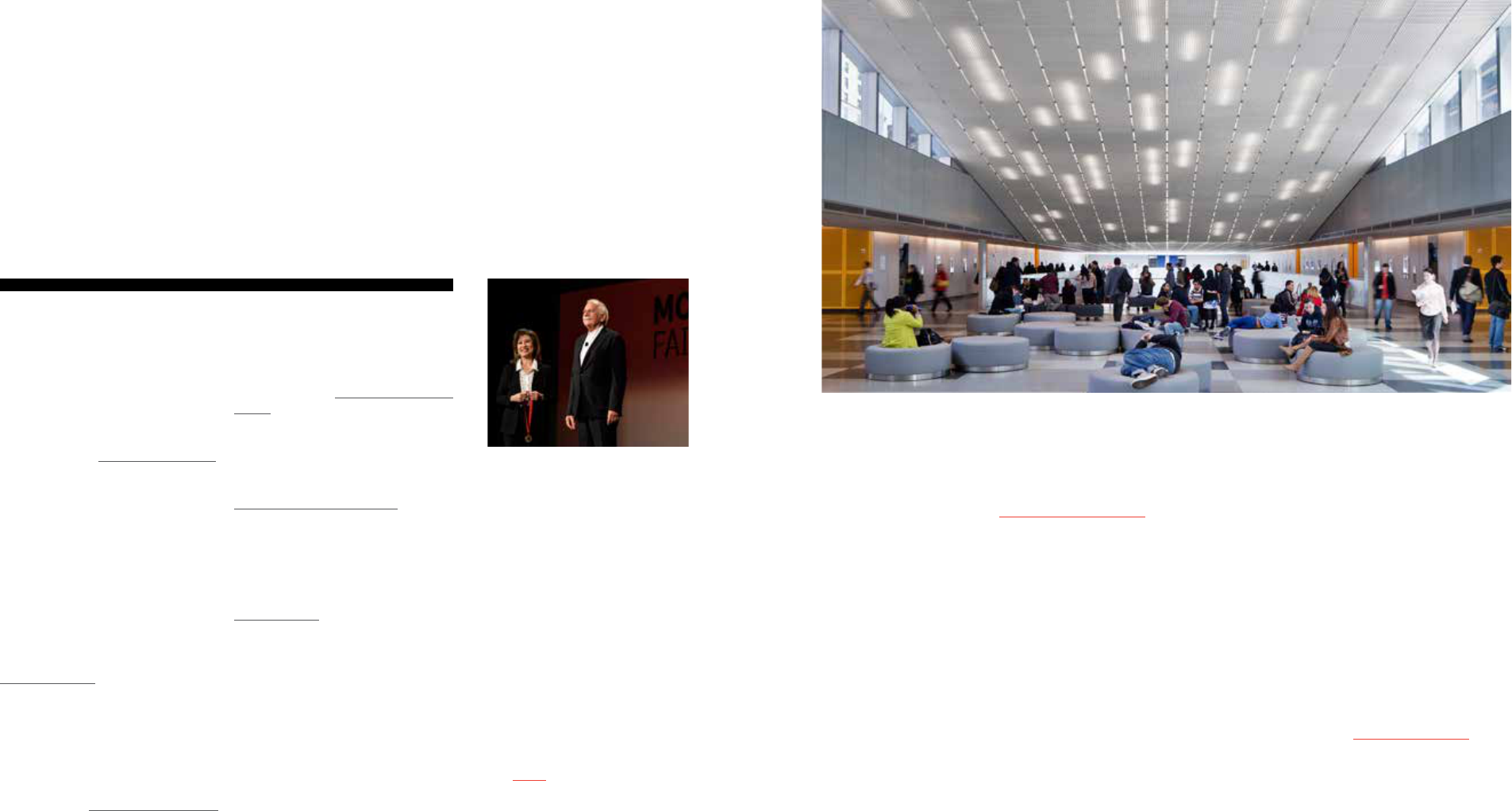

The AIA Convention 2015 in Atlanta delivered

on its billing. For nearly 17,000 attendees the

annual convention offered targeted seminars,

educational sessions and architectural tours.

Former President Bill Clinton delivered the

opening keynote, drawing a straight line from

what architects do to the needs of society. He

attracted the largest general session audience

in our convention history. Trending Topics

USA ranked #aiacon15 the nation’s eighth

most popular Twitter hashtag on May 14, the

opening of the three-day event.

Sustainable convention

The convention advanced AIA’s greening

initiative with a notable reduction in the

use of printed materials and increases in

recycling and waste diversion. Add to that the

attendees’ contributions to carbonfund.org

to offset 212.6 metric tons of CO

2

emissions.

Former President Bill Clinton shared his insights with attendees at

the AIA Convention 2015, calling on architects to do their best in

addressing the most pressing issues of climate change.

Photo credit: Carl Bower

AIA national staff manning the booth at Town Hall. Photo credit: Carl Bower

p // 192015 ANNUAL REPORTp // 18 THE AMERICAN INSTITUTE OF ARCHITECTS

Recognition

Recognizing excellence

We joined our members, the industry

and the media in celebrating some of the

world’s best new architecture, visionary

projects and up-and-coming architects

by awarding recognition across nearly

30 categories.

Our highest honor—AIA’s Gold Medal—

was awarded to Moshe Safdie, FAIA,

for the practice of architecture “in the

purest and most complete sense of the

word, without regard for fashion, with a

hunger to follow ideals and ideas across

the globe in his teaching, writing, practice

and research.” In his acceptance speech,

Safdie called for “a new urban vision”

in which city centers are reinvented

to integrate culture, commerce and

government and malls give way “to vital

and inclusive city centers worthy of our

civilization.”

Ehrlich Architects of Culver City, Califor-

nia, received the 2015 AIA Architecture

Firm Award. Ehrlich’s projects in the

American Southwest, the Middle East and

Africa are notable for blending classic

California modernist style with multicul

-

tural and vernacular design elements.

The 2015 AIA Twenty-five Year Award

recognized the distinctive façades of

Broadgate Exchange House in central

London, completed in 1990. Defined by

two parabolic arches against grids of

windows, the Skidmore, Owings & Merrill

design strategy was to vault 10 stories of

offices over rail tracks feeding Liverpool

Street Station. The result: a mid-century

modern icon.

The Rural Studio of Newbern, Alabama,

received the 2015 Whitney M. Young Jr.

Award for its work to design and build

homes and community buildings for west-

ern Alabama residents, almost 40 percent

of whom live below the poverty line.

Peter Eisenman, FAIA, was the 2015

AIA/ACSA Topaz Medallion recipient

in recognition of his writings, research

and scholarship and his commitment to

teaching.

COTE Top 10 for Students

The Committee on the Environment

(COTE) awards proved well-established

just one year in, drawing 400 entries from

40 schools. The 10 individual and student

team winners and their faculty advisors

addressed a challenging sustainable

design program, integrating natural

systems and technology to provide

architectural solutions to protect and

enhance the environment.

Practitioners

to watch

2015 Young Architects Awards

José Alvarez, AIA

An ardent advocate for design

excellence and a profession that

embraces diversity

Zachary R. Benedict, AIA

A leader who connects urban

sociology and social interaction

to show new roles architecture

can play

Hafsa Burt, AIA

A business owner, green building

advocate, mentor and exemplary

role model for architects

Justin Crane, AIA

An architecture festival creator

who connects the profession

with the public to deepen the

value of good design

Sarah W. Dirsa, AIA

An inspiring leader who gives

back to her community through

architecture

Andrew Dunlap, AIA

An intellectually curious designer

who leads by example

James Henry, AIA

A talented design principal

dedicated to advancing health

and wellness through design

Chris Hong, AIA

A capable leader committed

to helping others and

promoting architecture as a

public good

James A. Meyer, AIA

An advocate who harnesses

underutilized design profession

resources to enhance

stewardship of the public realm

Ann Sobiech Munson, AIA

A city council member with a

passion for broadening public

understanding of the profession

Adrianne Steichen, AIA

A committed leader and

advocate for affordable housing

Rebecca Talbert, AIA

An architect, educator and

advocate who leverages academic

expertise to effect real change

Derek C. Webb, AIA

An architect, educator and

mentor committed to the

professional development of

emerging professionals

Elizabeth Whittaker, AIA

An innovator helping pave the

way for other architects to

embrace the “maker” ethos of

the profession

2015 Associates Awards

Stephen Francis Gray, Assoc.

AIA

A community activist and leader

dedicated to improving the

built environment and helping

communities

Mary E. Hale, Assoc. AIA

An inspiring advocate for

improving the world through

architectural design and public

discourse

“I always tell my

students that if every

time they take a pencil

in hand to design,

if they can identify

completely with those

who will live, work and

be in their building, it is

half the way to victory.”

Moshe Safdie, FAIA, accepting the

2015 Gold Medal

2015 Honor Award for Architecture recipient John Jay College of Criminal Justice, designed by Skidmore, Owings & Merrill provides

all the functions of a traditional college campus within the confines of a single city block. The jury commented, “The diversity of

space is impressive, and it is hard to imagine that it could be done better.” Photo credit: Eduard Hueber | Archphot; Brett Beye

2015 AIA Gold Medal recipient Moshe Safdie

accepts the congratulations of colleagues

attending the AIA convention

Photo credit: Carl Bower

p // 212015 ANNUAL REPORTp // 20 THE AMERICAN INSTITUTE OF ARCHITECTS

Architects Foundation

Addressing local & global needs

In 2015, the Architects Foundation

worked to prepare tomorrow’s architects

for the challenges that lay ahead—

enhancing and expanding scholarships,

including the Diversity Advancement

Scholarship, which in addition to

financial support provides mentors and

professional training opportunities.

Through its major programs, the

Foundation advanced its efforts to

connect design professionals with the

immediate and long-term needs of

communities.

National Resilience Initiative

The Foundation’s National Resilience

Initiative (NRI) is building a nationwide

professional and academic network of

design programs that create community-

based resilience solutions. With support

from AIA, the Rockefeller Foundation’s

100 Resilient Cities, the Clinton Global

Initiative, Public Architecture, and the

Association for Collegiate Schools of

Architecture, the NRI added two design

studios: Mississippi State University’s Gulf

Coast Community Design Studio and

the University of Arkansas Community

Design Center. These centers offer design

services to households and communities

on issues ranging from hurricane

risks to the complexities of population

growth, transit-oriented development

and watershed urbanism. The goal is to

forge local solutions that are models for

mitigating social and disaster-related risk

around the globe.

Resilience & reconstruction

The Foundation partnered with the

relief organization All Hands Volunteers

to launch a three million dollar

reconstruction program for the villages

in Nepal devastated by the April 25,

2015 earthquake. The two-year initiative

includes coordinating with the Society of

Nepalese Architects (SONA), ARCASIA

(Architects Regional Council Asia) and

Small Works with the intention of building

up to 75 model homes compliant with

international model building codes and

increased resilience to natural disasters.

Training will be made available to

enhance Nepal’s design and construction

practices. The final phase will extend the

program into other Nepalese villages and

communities.

In communities from Nepal to Arkansas, the

Architects Foundation put its mission into

action, using the power of design to transform

lives, solve problems and create a better world.

The Architects Foundation launched a three million dollar reconstruction initiative in 2015 to rebuild

Nepalese villages and improve construction techniques in areas effected by a devastating earthquake.

Photo credit: Getty Images

p // 232015 ANNUAL REPORTp // 22 THE AMERICAN INSTITUTE OF ARCHITECTS

“ For the fifth year running, the American Institute

of Architects (AIA) has crunched the numbers on

its national sustainability challenge, the AIA 2030